Your Guide to Reducing Taxes in 2025 and Beyond

By: Brian Seay, CFA

The Super Bowl is over which means its tax time on the Capital Stewards Podcast. In this annual guide to taxes, I cover

Opportunities to reduce your 2024 taxes

Larger, long-term tax planning strategies

My view on tax policy and potential changes, including your “fair share” of the tax burden!

But first, let’s talk about those Super Bowl ads. I thought this year’s ads were better than last year, maybe an outlier opinion. Perhaps a comeback year for traditional categories like Trucks and Beer. I think my winner for best Ad goes to Ram Trucks with the Goldilocks and the Three Bears Ad. Perhaps second place to Budweiser, which I never thought I might say again, for a combination of the horse delivering the left behind keg and the ad about the Cul-de-Sac Party. Peyton Manning in a fanny pack is worthy of a mention all alone. Also, honorable Mention to Hellman’s Mayo, because as they say, it always hits the spot.

My vote for the worst Ad goes to the one I thought made the least business sense, which was Pizer’s ad, essentially just PR for the company. It seemed like a very expensive use of their capital, not memorable and it left me wondering what I was supposed to think about them as I watched the spot during the game.

All right, now that the Superbowl is over, lets turn to taxes.

Before we dive into strategies and ideas to reduce your 2024 taxes, it’s important to remember that tax reduction is a long-term game. Smart tax planning is not an annual hunt for deductions. That’s even more true now because the Trump Tax cuts, or the “Tax Cuts and Jobs Act,” increased the standard deduction, removed many of the more common itemized deductions and simplified the tax code. So that deduction hunt isn’t likely to be very fruitful. The bast ways to minimize taxes are through long-term strategies like

Investing in the right types of accounts (think retirement IRAs, ROTHs, 401ks),

Structuring your business entities appropriately (think S-Corps, Partnerships) and

Managing your taxable income through accelerations and deferrals

So if your “tax planning” is reduced to a deduction hunt each March, consider working with your CPA or financial advisor to create a more efficient, long-term tax plan. We would be happy to help! So more on those long-term strategies in a few minutes, let’s start with what you should consider turning the dial a bit to reduce your 2024 taxes.

Before we start looking for deductions, the first place to start is to identify opportunities to reduce your top line taxable income. Here are two strategies you may be able to use to reduce your income.

Reduce 2024 Taxable Income

Open a Heath Savings Account (HSA): If you have “material” medical expenses, which is virtually everyone, then an HSA is a great way to reduce your long-term tax liability. These accounts receive the “tri-fecta” of deductions. The contributions are tax deductible, the account grows tax-free, and distributions for healthcare expenses and some Medicare premiums are not taxed. Even if your medical expenses are not higher than 7.5% of income, an HSA may be a great tax reduction strategy. Similar to retirement accounts, you may still open and contribute to an HSA for 2024 until April 15th 2025.

Retirement Account Contributions: You have until the April tax deadline to contribute to retirement accounts for 2024. If your income was relatively high in 2024, consider making IRA contributions to receive a tax deduction now. However, we caution against doing this blindly every year. If your 2024 income was lower than usual, consider paying taxes now and receiving preferential capital gains tax treatment on future investment gains. Also, lower income years are great opportunities for ROTH conversions to minimize your total long-term tax liability. Remember, the IRS is in it for the long-haul, so you should be too!

Once we have reduced our income as much as possible, then it’s time to look for deductions and credits to offset taxes where possible. Here are four opportunities to help you offset your income from last year:

Maximize 2024 Tax Credits and Deductions:

Child Tax Credit…Don’t Forget Summer Camp: If you have children, you are eligible for a credit up to $2,000 until your income reaches $400,000 ($200,000 if single). Additionally, you can receive a credit for daycare, household help, and even day camps where children do not stay overnight. You may receive about 30% of your expenses up to $3,000 for one child or $6,000 if you have more than one child. So don’t forget those summer camp expenses.

Home Mortgage Interest: Home mortgage interest is one of the few deductions that remained after the tax law changes in 2017. However, interest is only deductible on balances below $750,000. As home prices have risen, particularly in large metro areas, more homes are crossing that threshold. The good news is that if you purchased your home before 2018, you are grandfathered into the old $1,000,000 limit.

Home Office Deduction: If you work from home as a requirement (i.e. not by your own choice) of your employment, then you may be eligible to deduct the cost of your home office. This includes pro-rata portions of mortgage interest, utility bills and depreciation.

Long-Term Care Insurance: Long-term care insurance premiums may be deductible as medical expenses when your total medical expenses are greater than 7.5% of your adjusted gross income. There are limits on the amount of premium that can be deducted, so check with your CPA when you file your taxes.

In addition to deductions and credits, there is one new change to think about for taxes this year and that’s a new 1099 you may have received for selling items online, like through Ticketmaster, StubHub or eBay.

In 2024, the threshold for reporting online transactions dropped from $20,000 to $5,000. Combine that with the increase in event prices (thanks Taylor Swift) and you might receive a 1099 from Ticketmaster, Ebay or some other online vendor where you made a transaction. If you sold something for a loss, like a secondhand item or a ticket you decided not to use, then you don’t owe tax. But if you made a profit, like on those Taylor tickets, then that’s the reportable income for your taxes!

Alright, so let’s shift gears and talk about longer term strategies where we can really move the needle on your tax bill.

Strategies for Reducing Taxes Long-Term:

Controlling Taxable Income:

Regardless of whether you own a business or are a highly compensated employee, you should attempt to control your taxable income. Controlling your income year after year allows you to smooth out years with usually high income that results in higher taxes. Here are a few ways to control taxable income:

Tax-Loss Harvesting: You may be thinking, “…but markets were up last year…” It’s unlikely that every single one of your investments increased in value throughout ALL last year. You should be selling losers to realize losses throughout the year so that you can use those losses to offset gains, even if total returns for the year are positive. This should be an every year strategy, not just a strategy for years with big losses.

Bunching Charitable Donations: If you normally give to charity each year, consider giving less in one year and substantially more in the next, especially if bunching your donations would allow you to give more than the standard deduction in a one year.

Control Business Income: If you are a partner or outright owner of a business, you may be able to influence whether the business pays income, realizes expenses, or sells assets in a given year. Managing your business income alongside your outside income can help lower your long-term effective tax rate and avoid “spikes” that lead to higher tax rates in one-off years. Your advisors should help you manage your total tax picture.

Net Investment Income (NIIT): If your Modified Adjusted Gross Income is above $250,000 (married) or $200,000 (single), you may be exposed to the Net Investment Income surtax of 3.8%. This also includes income from S-Corps for business owners if you aren’t meeting thresholds for active involvement. You may consider more active measures to control taxable income if you are hovering right around the NIIT thresholds.

Retirement Account Strategies to Reduce Taxes

We recommend clients have both ROTH and Traditional retirement accounts. You should look to fund ROTH accounts when income is relatively low and traditional accounts in high income years when the deduction is most valuable. Remember, taking a current year deduction and paying a higher rate down the road is not usually beneficial. Like all deductions, IRA deductions phase out as income grows, so discuss your retirement account contributions with your advisor on a regular basis. This is one area you should not “set and forget.”

Remember, if you own a business or are self-employed, you can contribute to your retirement account as both an employee and employer. This may enable you to defer upwards of $60,000 of income in some situations.

Real Estate Strategies to Reduce Taxes

Real estate can be a powerful tool for reducing your taxable income over the long-term, whether you are a business owner or an individual investor. This is especially true if you are married, and one spouse can work “full-time” in your real estate business to qualify as a professional. That allows the deductions from depreciation, mortgage interest, maintenance costs, management fees etc. to offset your other ordinary income.

You can also participate in a 1031 exchanges, which allows you to defer capital gains taxes when you sell a property by reinvesting the proceeds into a similar property. This strategy lets you continue growing your investment portfolio without the immediate capital gains tax hit. Again, the key is that someone needs to meet the qualifications as a real estate professional and you need to be able to focus on individual properties or private funds and not publicly traded REITS.

Changes to Trump Tax Cuts for 2025

This year, in addition to simply planning with the tax regime we have in place, we also need to consider the potential for tax changes at year end with the expiration of the Trump Tax Cuts and Jobs Act from 2017. So, in this episode, I’ll start with the tax planning strategies you need to know, and then round out the discussion with my views on potential changes to tax policy going forward.

It's helpful to look at the outlook for tax changes from Washington because they could be very impactful going forward. In 2017, during his first Presidency, Trump passed the Tax Cuts and Jobs Act (TCJA). That bill increased the standard deduction, eliminated some long-standing itemized deductions, simplified tax preparation and lowered taxes across the board. If the existing cuts are not extended, it would amount to the largest year over year tax increase for Americans in history. So despite all of the arguing, my view is that the majority of the 2017 tax cuts will be extended going forward. No democrat or republican, no matter how fiscally conservative, wants to be responsible for that kind of effective tax increase. And I think when we look at some recent data, you will see why a tax hike, on any group doesn’t make much sense.

Anytime we talk tax policy, I like to ground everyone, which is hard because you will not get that on the evening news. Here are three charts that may help you understand how taxes work today in America.

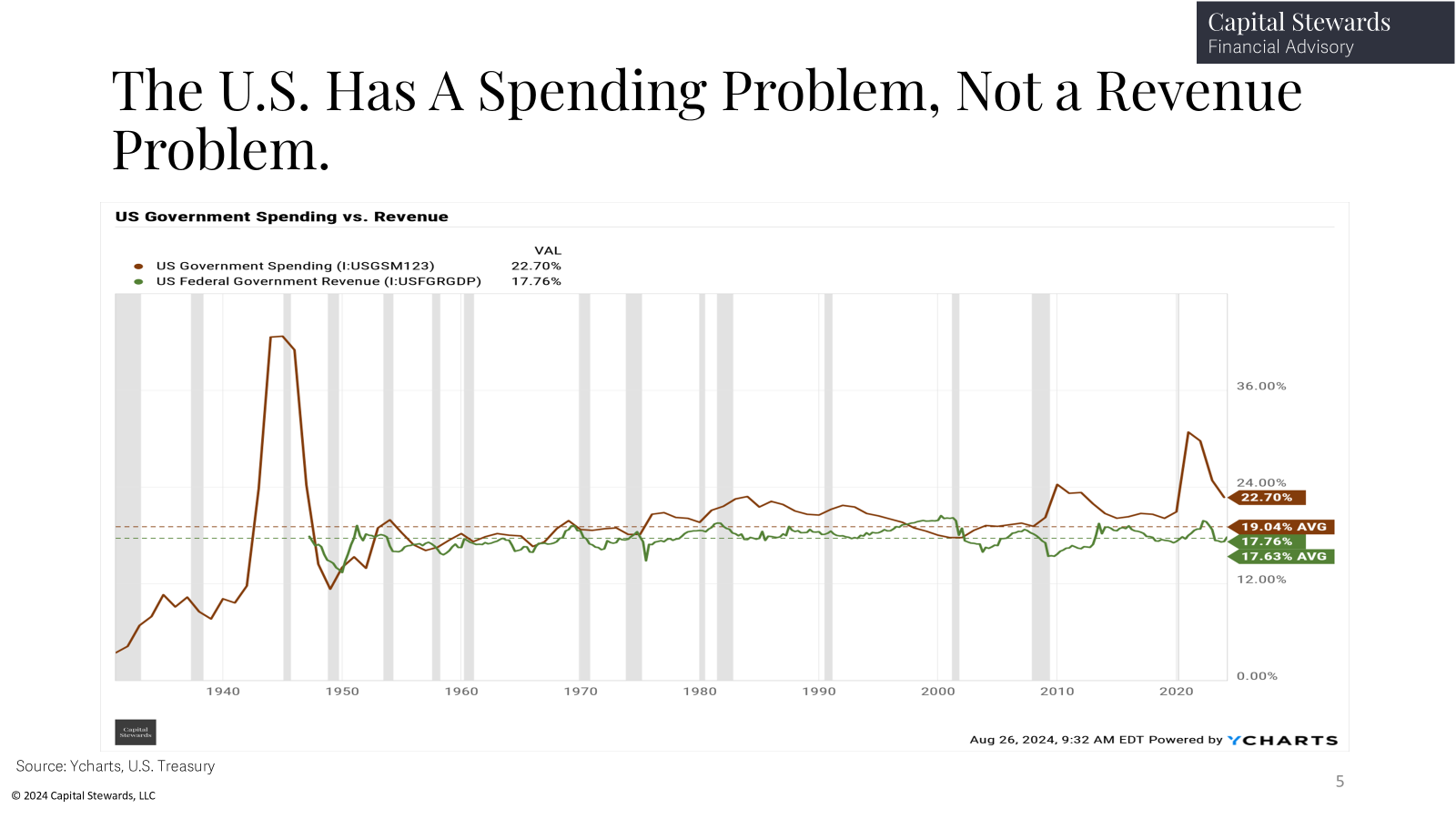

First, it’s clear that we have a spending problem, not a revenue, or a “tax” problem. You can see on the chart, going back to the 1950s, taxes were about 17% of GDP and that green line has been very consistent over time. The red line, which is spending, has ballooned up in recent years. Spending should be closer to 17% to 18% of GDP and our budget should be close to in balance every year. Instead, we have spending north of 22% and a big deficit and debt problem. Regardless of your politics, the line that has changed recently is the spending line, not the revenue line.

Second, taxes in the U.S. are mostly paid by rich people. Shocker I know.

The top quintile, or the top 20% of income earners, is literally the only group that pays a higher percentage of the taxes than their share of the income. They are the only group that pays their "fair share" by the numbers. You can see on the chart, the middle quintile makes $83,100. They earn 14% of the all of the income. But they only pay 9% of the taxes. If the system was totally “fair” to everyone, they would pay 14% of the taxes, but they do not. You can clearly see, the lower your income, the lower your share of taxes. That’s called a progressive tax code, which means the highest income earners pay most of the taxes. You can see on the chart, the highest income earners earn 55% of the income, but they pay 69%, more than 2/3s, of the total taxes, or more than there “share” of the income taxes.

Now, you can make a political statement that they should pay more, but then you need to define what “more” means. Because the wealthiest people in the U.S. already pay more than their “fair” share of the taxes. So it’s not logically sound to say “the rich” or “billionaires” don’t pay their “fair share.” They objectively pay more than their fair share of the taxes.

The other popular argument is that “rich people” pay lower effective tax rates than their secretary – the famous Buffet example. Contrary to what you hear on the news, the top quintile pays a higher average tax rate than all of the other quintiles and you can see that as your income moves higher, your average tax rate goes up.

The other point I’ll make here is about the top 1% since that gets so much airtime. If I broke out the top 1% here, it wouldn’t look any different. They pay more of the taxes than their income would dictate and their tax rates are higher than the other groups in the top quintile, so there isn’t any funny business going on at the tip top of the chart.

For fun, I ran the numbers on what it would take to balance the Federal deficit and only increase taxes on the top 5% - which right now is those with income over $330,000, the effective tax rate on those income earners would have to be 69%. That means a statutory rate of probably close to 100% to allow for deductions etc. So it sounds good to say that we should solve our problems by increasing taxes on the small number of families in the top income brackets, but there simply isn’t enough money to for that to be a workable solution.

Now that you have a picture of who pays what now, let’s look at what changes are on the table and what’s at risk in the negotiation for the tax package for next year. As I mentioned earlier, I expect most of the existing cuts to remain, though one or two might be sacrificed or adjusted to get the bill passed. Here are a few areas that I would watch over the course of the year:

The qualified small business income deduction. This is hugely important for small business owners because it allows them to deduct 20% of their income or profits right off the top on their tax bill.

The State and Local Tax Deduction, or the SALT deduction. Right now, the cap on deducting state and local taxes from your federal taxes is $10,000. I expect that to go higher to appease Republicans in New York and California, which they need to get the tax bill passed.

The third item is the estate tax. That limit was increased from around $5 million to the current almost $14 million dollar threshold per person. We could see that limit move lower to include more families and raise more revenue as part of negotiations.

Lastly, the top marginal rate, which is currently 37%, could be increased. Despite my arguments above, this is always the most politically popular way to raise revenue because it impacts the fewest people.

I’m more skeptical on further cuts than some. The President campaigned on further reductions to the corporate rate, eliminating taxes on social security and eliminating taxes on tips for service industry workers. Those cuts would likely need to be funded either by spending reductions or tax increases elsewhere. Eliminating social security taxes in particular lead to a significant reduction in revenue that the deficit hawks in the republican party may not like. I’m assuming Trump will get at least one of these in the bill, but it would surprise me if he got all three. Again, revenue today is consistent with historical levels, so there isn’t a need for significant tax reductions.

As we go through the year, we will keep you updated on how changes might impact your planning and steps you might need to take before year end. I do think this is a year where year-end tax planning may be more important than usual because changes in the code may create opportunities that you need to take advantage of before the calendar flips to 2026.

So in closing, if you remember nothing else, remember that Taxes are a long-term game. The most important things you can do are those long-term strategic choices we discussed. Structure your business entities correctly, contribute to the right kind of retirement account and evaluate those decisions every year. The difference can add up to hundreds of thousands of dollars over many years, far more than a few extra deductions for 2024 or 2025. If you have questions about tax planning, or about integrating your tax planning with your investments, then reach out anytime, I would be happy to discuss further.